The year 2021 brought new challenges to the auto insurance industry—from frequent shifts in miles driven to significant staffing shortages. As we enter 2022, insurance carriers will need to manage many of these trends expected to continue. To help you prepare and navigate what’s next, here are Enlyte’s top 2022 predictions:

- Miles Driven Will Fluctuate; Severity Will Continue to Rise

- Provider Demographic Data Will Remain a Focus

- Increased Technology Use, Automation Will Continue, Especially Amid Staffing Shortages

- The Quick Pace of Regulatory Change Will Continue

- Prescription Management, Driving Under the Influence Will Continue to Be a Focus

Miles Driven Will Fluctuate; Severity Will Continue to Rise

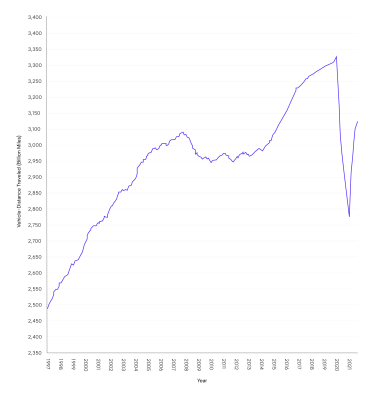

While there was an uptick in number of miles driven in 2021 compared to 2020, according to the U.S. Department of Transportation, that factor has still not returned to pre-COVID-19 levels. Since the start of the pandemic, we have seen a demonstrable correlation between employees working remotely and miles driven. We expect the work-from-home trend to continue—between May and September 2020, about half of the workforce worked remotely either some or part of the time. The same study found that 91% of those workers hope their ability to work remotely continues after the pandemic.

Source: U.S. Department of Transportation

As employers finalize their long-term remote work policies, new COVID-19 variants emerge and the pandemic situation continues to evolve, we expect miles driven to continue to fluctuate and don’t anticipate that the United States will return to pre-pandemic driving levels in 2022.

While miles driven will continue to change throughout the year, claim severity is on the rise for both first-and third-party claims. We expect this trend will continue, driven mostly by medical costs due to increased emergency room frequency and more expensive pain-management techniques and outpatient surgeries.

“The shift to work from home will continue to impact miles driven indefinitely. The pandemic has demonstrated how quickly, easily and effectively moving to the work-from-home model can be. Expectations have now been set for the current and future workforce. As the impact of the pandemic wanes, there will be an increase in travel and miles driven. However, metrics will not return to pre-pandemic levels outside of normal population growth." —Mike McKinley, Director of Product Development, Coventry

Provider Demographic Data Will Remain a Focus

In the auto casualty sector, networks will continue to evolve from changes brought by the pandemic. In some cases, the response to these challenges will mean expanding network coverage to ensure access to care that is medically sound and available as needed. To better weather the economic upheaval of the past two years, some providers retired whereas others have moved where they practice or joined physician groups. Changes among providers who have been reacting to a difficult couple of years by shifting how and where they practice, or even giving up practicing altogether, will raise challenges around demographic data accuracy.

Restrictions brought by COVID-19 and the resulting economic hurdles mean some providers will continue to adopt changes. Capturing these shifts will require continued efforts around gathering accurate provider data. A shortfall of providers—a preexisting condition the nation faced even before the pandemic—will remain a major challenge. Among those providers who remain, education will remain essential when it comes to shifts in regulations.

Increased Technology Use, Automation Will Continue, Especially Amid Staffing Shortages

Though we might never see the rapid rate of technology adoption that occurred at the start of the pandemic, we expect that auto insurance carriers will continue to look to technology to help ease or solve many of the lingering pandemic-related challenges that carriers still face.

For the past few years, the insurance industry has experienced a talent crisis due to its aging workforce, and the pandemic has only magnified the issue. In November 2021, 4.5 million people quit their jobs according to the Bureau of Labor Statistics, and a recent study of the insurance market found that many insurance professionals are exploring career changes and “reevaluating” their current roles.

We expect this labor trend—what many have dubbed “The Great Resignation”—will drive significant technology adoption in 2022. Specifically, we predict insurance carriers will focus on applying it in three areas:

- Boosting Efficiency: Automation, no-touch claim processing and artificial intelligence will be top of mind for insurance carriers experiencing staffing shortages.

- Training: Using technology to not only train new adjusters quickly, but also offer insights and red flags to help them in real-time.

- Retaining Internal Expertise: Many carriers will focus on integrating the knowledge of their top adjusters and claim specialists into their technology platforms to reduce the risk of that information being lost as those employees change jobs or retire.

While staffing shortages may be one of the top drivers of technology use and adoption in 2022, carriers will also turn to new technologies to help improve outcomes and create better policy holder experiences.

“I expect to see an increase in using machine learning and artificial intelligence to automate more of the claims process as a means to improve policy holder experience.”—Bob Acosta, Senior Vice President of Sales, Enlyte

The Quick Pace of Regulatory Change Will Continue

In 2021, the auto casualty industry experienced one of the most active regulatory and legislative landscapes in years, driven by emergency COVID-19 regulations and the major fee-schedule change in Michigan. Our regulatory experts don’t see this activity slowing down anytime soon.

In 2022, some of the top regulatory and legislative issues will include:

- COVID-19-Related Changes: As the pandemic situation continues to change, we expect to see regulatory and legislative shifts related to COVID-19 that affect the auto insurance industry.

- Florida PIP: In 2021, the Florida legislature passed a bill that would eliminate the state’s Personal Injury Protection (PIP) system. While that bill was ultimately vetoed by the governor, in 2022, we expect there to be continuing efforts to eliminate PIP, especially as we’ve seen an increase in litigation related to the current system.

- Michigan No-Fault Fee Schedule: Last year, a new Michigan fee schedule went into effect. Though there have been requests from multiple parties involved, from carriers to providers, our experts don’t expect the Michigan regulators to make any changes to the fee schedule in 2022. Instead, we anticipate that the state will be watching closely to judge how the fee schedule is working during its first full year of implementation.

- Medical Marijuana: We do not believe the FDA will approve the use of medical marijuana at a federal level in 2022, rather it will be delayed until 2023 due to other priorities. We are also watching closely as Congress discusses de-scheduling recreational marijuana as well. This will have significant effects for auto insurers, especially when it comes to understanding the correlation between impairment and crashes and injuries, identifying the best methods to determine intoxication and sorting out coverage of medical marijuana for claimants injured in auto accidents. Any changes by the federal government will speed up the national conversation about reimbursement, banking, impairment and insurability.

- Social Inflation: The effects of social inflation on claim settlements have been at historic levels. Litigation funders capitalizing on large settlements are at the forefront and the industry is interested in disclosure of funding agreements and caps in the amounts awarded. Approximately a quarter of district courts require the disclosure of funding agreements in litigation cases today, a number we will likely see expand in 2022 or 2023.

- Payer Legislation: In 2021, many states began implementing legislation that directly affects carriers’ ability to manage claims. For example, this might involve introducing new administrative rules that can result in more administrative tasks and increased costs. We believe this trend will continue.

- Data, Privacy & Security: There will be a continued focus on medical data security as many regulators evaluate the effectiveness of their current privacy and security laws regarding issues such as how medical data is accessed and how claims are paid.

“With continued regulatory updates related to the pandemic, auto-liability issues, major fee schedule changes on the horizon and an active discussion about marijuana at the federal level, 2022 will be another busy year for the auto insurance industry’s legislative and regulatory landscape. Claims performance and severity issues will continue to drive our regulatory landscape in 2022.”—Michele Hibbert, Senior Vice President, Regulatory Compliance Management

Prescription Management, Driving Under the Influence Will Continue to Be a Focus

Pharmacy-related auto concerns will not only involve appropriate prescription management and monitoring this year, but will more comprehensively involve overutilization of specialty and compounded medications, while considering other factors.

Despite decades of safety gains within the auto industry, the latest findings suggest the pandemic has made drivers more likely to drink alcohol and use drugs. But it is not only alcohol and illicit substances we should be concerned about. Medications commonly prescribed to patients can also impair driving. According to the National Highway Traffic Safety Administration (NHTSA) “10% of weekday, daytime drivers surveyed tested positive for prescription and/or over-the-counter drugs”, which could include medications commonly known to cause impairment such as antianxiety medications, antidepressants, antihistamines, antihypertensives and benzodiazepines. Annual prescribing of opioids, often prescribed for pain, are decreasing. However, the widespread identification of prescription opioids in fatally injured drivers is on the rise. Pharmacists and PBMs are in a unique position to assist combating the growing problem of driving under the influence of drugs (DUID) by providing patients with counseling and education in combination with the PBM’s ability to monitor drug interactions, manage prescriptions and recognize risks.

Adding to impairment concerns, there has been significant legislative activity around marijuana—both medical and recreational—across the country. One study found that in states with legalized marijuana, crashes increased by 5.2%–6% in comparison to states without legalized marijuana. Another study found accident-causing drivers were three to seven times more likely to have tetrahydrocannabinol (THC) in their blood. While not all accidents reported in the study involved medical marijuana, whose use in PIP coverage is being considered in some states, the findings reflect growing concerns for the auto casualty industry, especially as more states continue legalization efforts in 2022.

Common injuries sustained in car accidents such as whiplash, back injury and head trauma are often associated with chronic or acute pain. For these types of injuries, prescription opioids, such as oxycodone and hydrocodone, which are widely used for pain management, may be prescribed. Given this, the greater need for pain management is increasingly creating a demand for more aggressive clinical intervention that ensures appropriate and cost-effective care. To address this, auto-specific PBMs are becoming more important than ever in monitoring prescription regimens.

In addition to these concerns, auto casualty faces issues like those seen in workers’ compensation, including the need for greater drug pricing transparency and regulatory oversights to address increasing drug prices.

Looking Ahead

Though it is challenging to predict exactly what will be the most significant trends, cost drivers and changes in the auto insurance industry in 2022, carriers can be prepared for whatever comes next by keeping an eye out for the issues listed above.